Published on: 2024-08-10 18:37:05

In consumer lending, decision-making centers on several areas: anti-fraud, loan underwriting, credit limit setting, cross-/up selling, portfolio management, and debt recovery. A data-driven company can automate each area with the help of a decision engine.

If you are new to consumer lending and plan to set up a consumer lending business, you can learn more from our overview.

This hub covers topics related to decision-making across key areas of consumer lending.

Anti fraud

Loan underwriting

Portfolio management

Data Analytics

Related Articles

-

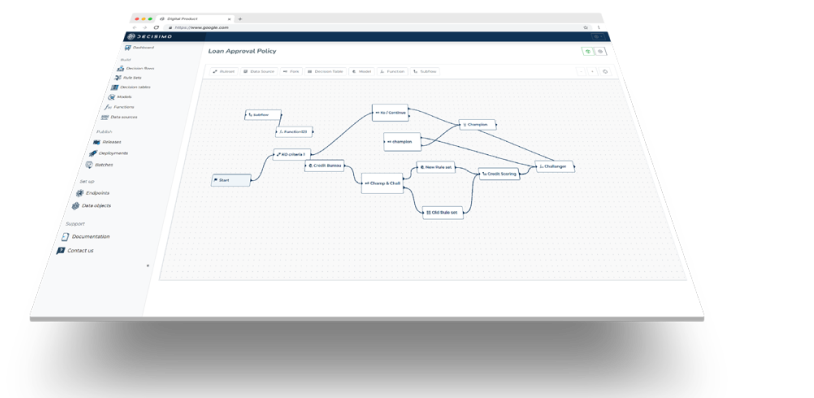

Step-by-Step Guide to Automating the Loan Approval Process

Automating this process is necessary to keep up with industry demand. It also improves the accuracy and efficiency of your operations.

-

Decision Strategy in Scaled Lending: How to Manage Decision Logic Without Destabilizing Growth

In scaled lending, decisioning is not just about approving or declining applications. It shapes credit losses, collections inflow, funding needs, operational load, and the stability of the business. A sound decision strategy starts with situational awareness, defines a clear end goal, and models the downstream impact of every change before it goes live.

-

Stopping Synthetic Identity Fraud with SEON and Decisimo - Decisimo

Synthetic identity fraud exploits small gaps in identity data. This article explains how SEON adds digital footprint and address analysis to registration checks, and why that mix helps businesses spot suspicious identities before they open an account or complete a purchase.

-

Bridging Manual and Automated Scoring Models

Manual scoring models used statistical scorecards but slowed decision-making with time-consuming data work. This article explains how machine learning-based automated scoring speeds evaluations and improves accuracy, and why causal analysis and second-order effects matter when you implement decision logic and decision workflows.

-

Attribute and Model Management: How to Track Stability Without Weakening Your Decision Strategy

Adding more attributes to a model does not always improve decision quality. If predictors are poorly grouped, weakly represented, or unstable over time, they can degrade model performance and create risk for the wider decision strategy. This article explains how to manage attributes and models with stability in mind, and why binning and categorizing predictors remains a practical way to keep automated decisions explainable, traceable, and reliable.

Preventing Identity Fraud

Preventing Identity Fraud