Why Complex, Branching Rules Put Your Business at Risk - Decisimo

Published on: 2024-08-10 18:36:09

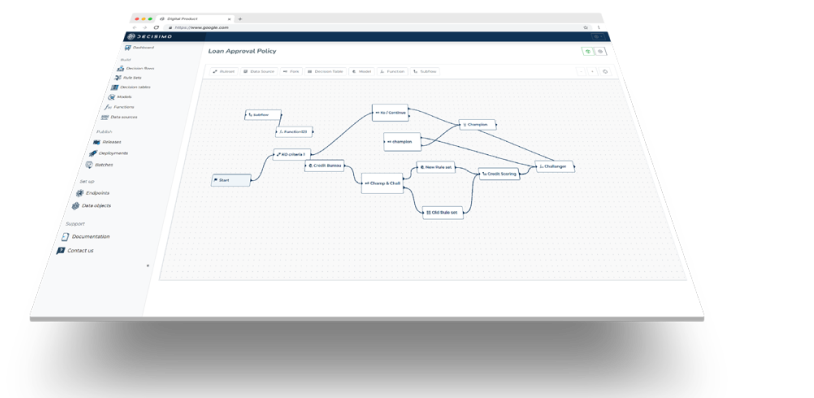

As businesses grow, their decision-making processes often become more complex. Many organizations use decision management platforms like Decisimo to set up rules for those processes.

But complex, branching rules are often the wrong approach. Here is why:

Drawbacks of Complex, Branching Rules

Branching rules are hard to maintain. They are often difficult to understand and include many interdependent parts.

That complexity makes it hard to track which rules are active, what they do, and why they were created. This can lead to mistakes when teams modify or update the rules.

Complex rules can also hide important business terms that should be defined clearly. When that happens, teams may interpret the same logic differently.

Testing and debugging these rules is harder as well. It is often difficult to find issues inside a web of connected conditions, which leads to slow and expensive fixes.

Modular Rules: A Better Alternative

Instead of building a maze of complex rules, use a modular approach. Break down complex logic into smaller, easier-to-manage pieces.

This makes each rule clear and easier to maintain, with terms that teams understand the same way. Smaller rules are also easier to test and debug, which speeds up issue resolution.

Advantages of Modular Business Rule Management

Complex rules may look effective at first, but they often create more risk than value. They are harder to maintain, can blur key business terms, and make debugging harder than it should be.

A modular setup makes rules easier to understand and maintain. It creates a clearer, more efficient system for decision-making.